In international trade, project finance, contract execution, and large-scale commercial transactions, financial security remains a primary concern. Buyers want assurance that suppliers will perform. Sellers want certainty that payment obligations will be met. Lenders want protection against default risks.

This is where an SBLC (Standby Letter of Credit) becomes one of the most valuable financial instruments in modern business.

Whether you’re involved in international trade finance, construction contracts, commodity transactions, infrastructure projects, import-export business, or corporate financing, understanding how an SBLC works can help reduce risk, improve credibility, and unlock larger opportunities.

In this comprehensive guide, you’ll learn:

- What an SBLC is

- How a Standby Letter of Credit works

- Types of SBLCs

- Benefits and risks

- Real-world applications

- A practical case study

- Frequently asked questions

- How businesses use SBLCs to secure transactions

Primary Keyword: What is SBLC

LSI Keywords:

- Standby Letter of Credit

- SBLC financing

- SBLC for international trade

- Trade finance instruments

- Bank guarantee vs SBLC

- Financial Standby Letter of Credit

- Performance SBLC

- SBLC MT760

- International trade finance solutions

- Credit enhancement instruments

What Is SBLC?

A Standby Letter of Credit (SBLC) is a financial guarantee issued by a bank on behalf of a customer. The bank commits to pay a beneficiary if the applicant fails to fulfill contractual or financial obligations.

In simple terms, an SBLC acts as a backup payment mechanism.

Instead of serving as the primary payment method, it provides assurance that payment will occur if the obligated party defaults. According to global banking practices, an SBLC represents an independent undertaking by the issuing bank to honor valid claims made under the terms of the instrument.

Businesses worldwide use SBLCs to support:

- International trade transactions

- Construction projects

- Commodity trading

- Equipment procurement

- Infrastructure contracts

- Corporate financing

- Investment transactions

Because banks stand behind the obligation, beneficiaries gain confidence in the transaction.

How Does an SBLC Work?

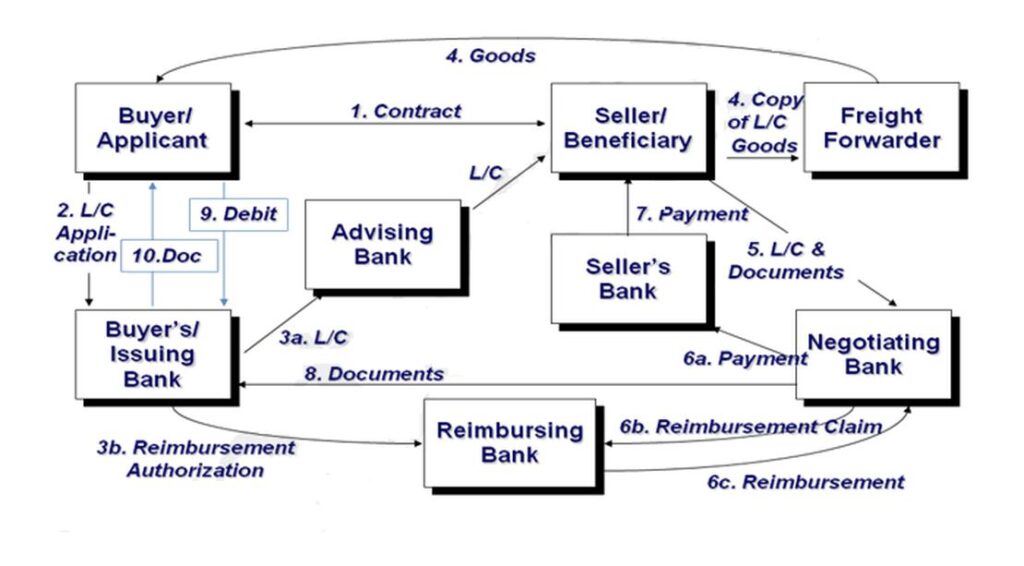

Every SBLC transaction typically involves three parties:

1. Applicant

The party requesting the SBLC.

2. Issuing Bank

The financial institution issuing the SBLC.

3. Beneficiary

The party receiving the guarantee.

Step-by-Step Process

Step 1: Contract Agreement

Two businesses enter a commercial agreement.

Step 2: SBLC Requirement

The beneficiary requests an SBLC as security.

Step 3: Bank Assessment

The issuing bank evaluates:

- Creditworthiness

- Financial capacity

- Business performance

- Available collateral

Step 4: Issuance

The bank issues the SBLC.

Many international transactions utilize SWIFT MT760 messaging for issuance and transmission.

Step 5: Contract Performance

The applicant performs contractual obligations.

Step 6: Claim Event

If the applicant defaults, the beneficiary submits required documents and claims payment according to SBLC terms.

Step 7: Bank Payment

Upon verification of compliant documentation, the issuing bank honors the claim.

Why Businesses Use SBLCs

Companies use SBLCs because they reduce transaction risk.

Major benefits include:

Enhanced Credibility

Businesses can demonstrate financial strength and reliability.

Reduced Counterparty Risk

Beneficiaries receive assurance from a bank rather than relying solely on the applicant.

Increased Contract Opportunities

Many government contracts and international tenders require financial guarantees.

Improved Trade Relationships

Suppliers and buyers gain confidence when an SBLC supports the transaction.

Better Financing Options

Banks and investors often view SBLC-backed transactions more favorably.

Types of SBLC

Financial SBLC

A Financial Standby Letter of Credit guarantees payment obligations.

If a buyer fails to pay, the bank pays the beneficiary.

Common uses include:

- Import-export transactions

- Commodity trading

- Corporate purchases

- Supplier agreements

Performance SBLC

A Performance SBLC guarantees contractual performance.

If a contractor fails to complete work according to contract terms, the beneficiary may claim compensation.

Common uses include:

- Construction projects

- Infrastructure development

- Engineering contracts

- Manufacturing agreements

Advance Payment SBLC

Protects buyers who make advance payments.

Bid Bond SBLC

Supports participation in competitive tenders.

Direct Pay SBLC

Provides a direct payment undertaking under specified conditions.

Commercial SBLC

Used for complex trade finance structures.

SBLC vs Letter of Credit

Many business owners confuse an SBLC with a traditional Letter of Credit (LC).

Letter of Credit

A standard LC serves as a payment mechanism.

The seller receives payment when shipping documents meet LC requirements.

SBLC

An SBLC functions as a contingency instrument.

Payment occurs only if the applicant fails to perform contractual obligations.

| Feature | Letter of Credit | SBLC |

|---|---|---|

| Primary Function | Payment Tool | Guarantee Tool |

| Payment Trigger | Document Presentation | Default Event |

| Trade Usage | Frequent | Backup Protection |

| Risk Coverage | Transaction Risk | Performance Risk |

SBLC vs Bank Guarantee

Although both instruments provide security, differences exist.

Bank Guarantee

A bank guarantee typically compensates a beneficiary after default under applicable terms.

SBLC

An SBLC operates under internationally recognized documentary rules and often follows:

- ISP98

- UCP 600

These frameworks standardize international banking practices.

Industries That Commonly Use SBLCs

International Trade

Importers and exporters frequently require SBLCs.

Construction

Large projects often require performance guarantees.

Energy

Oil, gas, renewable energy, and power projects use SBLCs extensively.

Manufacturing

Equipment suppliers often request financial security.

Infrastructure

Governments and private developers use SBLCs for project assurance.

Commodity Trading

SBLCs help secure large-value transactions involving:

- Gold

- Silver

- Agricultural products

- Petroleum products

- Metals

Advantages of an SBLC

Strengthens Business Reputation

Companies gain credibility when reputable banks support transactions.

Facilitates International Trade

Businesses can transact across borders with greater confidence.

Reduces Default Risk

The issuing bank provides an additional layer of security.

Supports Growth

Organizations can pursue larger contracts and projects.

Improves Supplier Confidence

Suppliers feel more comfortable extending credit terms.

Flexible Financial Instrument

SBLCs support multiple business sectors and transaction structures.

Risks and Considerations

While SBLCs provide significant benefits, businesses should evaluate:

Issuance Costs

Banks charge fees based on:

- Credit profile

- Transaction size

- Risk level

- Duration

Documentation Requirements

Errors in documentation may affect claims.

Expiry Dates

Failure to monitor expiration dates can create exposure.

Regulatory Compliance

International transactions require compliance with banking regulations and sanctions requirements.

Credit Evaluation

Banks assess applicants thoroughly before issuance.

Real-World Example of an SBLC

A manufacturing company in Germany agrees to purchase industrial equipment from a supplier in Singapore worth $5 million.

The supplier has never worked with the buyer before.

To reduce payment risk, the supplier requests an SBLC.

The buyer’s bank issues a Financial SBLC for the contract value.

The supplier proceeds with production and shipment.

If the buyer pays according to contract terms, the SBLC expires unused.

If the buyer defaults, the supplier can submit a compliant claim and receive payment from the issuing bank.

The transaction proceeds smoothly because both parties trust the security provided by the SBLC.

Case Study: Infrastructure Project Financing

Background

A regional government awarded a $150 million infrastructure contract to a construction company.

The government required assurance that project milestones would be completed on schedule.

Challenge

The government needed protection against:

- Delays

- Non-performance

- Contract breaches

Solution

The contractor obtained a Performance SBLC from a leading international bank.

Outcome

The government gained confidence in project execution.

The contractor secured the contract.

The project achieved completion within the agreed timeline.

The SBLC remained unused because contractual obligations were fulfilled.

Key Lesson

In many commercial transactions, the true value of an SBLC lies in the confidence it creates rather than the payment it provides.

International Rules Governing SBLCs

Most SBLCs operate under internationally accepted standards.

The most common include:

ISP98

International Standby Practices establish specialized rules for standby letters of credit.

UCP 600

Uniform Customs and Practice for Documentary Credits also governs certain SBLC structures.

These frameworks provide consistency and predictability in global trade finance.

Best Practices When Using an SBLC

Work With Experienced Financial Institutions

Choose banks and financial partners with proven trade finance expertise.

Review Documentation Carefully

Clear wording reduces disputes.

Verify Beneficiary Requirements

Understand claim procedures before issuance.

Monitor Expiration Dates

Track all renewal and maturity deadlines.

Seek Professional Guidance

Complex transactions often require specialist advice.

External Resource

For additional information on Standby Letters of Credit and international trade finance, visit:

ICC Academy – Comprehensive Guide to Standby Letters of Credit

ICC Academy Guide to Standby Letters of Credit

This resource provides extensive insight into SBLC structures, rules, and applications.

Frequently Asked Questions (FAQ)

1. What is the main purpose of an SBLC?

An SBLC provides financial security by guaranteeing payment if the applicant fails to meet contractual obligations.

2. Is an SBLC the same as a bank guarantee?

No. Although both provide security, SBLCs typically operate under international documentary credit rules and function as independent payment undertakings.

3. Who can apply for an SBLC?

Businesses, corporations, traders, contractors, and project developers with sufficient financial standing can apply through a bank.

4. How long does an SBLC remain valid?

Validity periods vary depending on transaction requirements. Some remain active for several months, while others extend for multiple years.

5. What is MT760 in SBLC transactions?

MT760 is a SWIFT message format commonly used to issue and transmit bank guarantees and Standby Letters of Credit.

6. Can an SBLC be used for project financing?

Yes. Many infrastructure, construction, energy, and investment projects use SBLCs as credit enhancement instruments.

7. What documents are required for an SBLC?

Requirements vary by bank but generally include corporate documents, financial statements, contract details, and credit assessments.

8. Is an SBLC transferable?

Transferability depends on the wording and terms specified within the instrument.

Final Thoughts

A Standby Letter of Credit (SBLC) remains one of the most trusted financial instruments in global commerce. By providing a bank-backed guarantee, it strengthens confidence between trading partners, reduces financial risk, supports project execution, and enables businesses to secure opportunities that might otherwise remain inaccessible.

Whether you’re involved in international trade, construction, commodity transactions, procurement, project finance, or corporate funding, understanding how SBLCs work can help you structure transactions more effectively and protect your commercial interests.

As global markets become increasingly interconnected, businesses that leverage financial instruments such as SBLCs position themselves for stronger growth, improved credibility, and greater transactional security.

#SBLC #StandbyLetterOfCredit #TradeFinance #InternationalTrade #ProjectFinance #BankGuarantee #FinancialInstruments #ImportExport #BusinessFinance #CorporateFinance

READY TO SECURE YOUR NEXT TRANSACTION?

At Baili Finance Limited, we help businesses access professional trade finance solutions designed to support growth, strengthen credibility, and reduce commercial risk.

Whether you need:

✅SBLC Issuance Assistance

✅Trade Finance Solutions

✅Project Finance Support

✅Bank Guarantees

✅International Transaction Structuring

✅Corporate Funding Solutions

Our specialists are ready to help.

Contact Baili Finance Limited Today

Don’t allow financing barriers, transaction risks, or credibility concerns to delay your next opportunity.

🌐www.bailifinancelimited.com

Speak with our trade finance experts now and discover how an SBLC can unlock larger contracts, safer transactions, and stronger business growth.

Contact us today and let’s structure a solution that works for your business.

Intermediaries/Consultants/Brokers are welcome to bring their clients 100% protected. Our brokers receive 2% commission for referral. We assist Clients and brokers in their attempt to secure funding by working on their funding requests that may require innovative financing. In complete confidence, we will work together for the benefits of all parties involved.